IRS WASH SALE RULE EXPLAINED:

A TRADER’S DEEP DIVE

Demystifying the IRS Wash Sale Rule and Its Impact on Your Taxable Gains

In our article, What is a Wash Sale?, we explained the fundamentals of what a wash sale is and why the Internal Revenue Service (IRS) is concerned with them. Now, we’ll dive into the details of the IRS Wash Sale Rule. Codified as Section 1091 of the Internal Revenue Code, this regulation is notoriously complex. While IRS Publication 550 offers guidance, the rules have evolved over a century, leaving some aspects vague and confusing.

To help you understand how this rule impacts your bottom line as an active trader, let’s break down the essentials of the IRS Wash Sale Rule into everyday language.

Rather watch than read? Here’s a video version:

1. The 61-Day Window: How the IRS Defines a Wash Sale

The most basic component of the IRS Wash Sale Rule is the timing window. The IRS states that if you sell a security at a loss and then replace it within a window that spans 30 days before the loss and 30 days after the loss, it is considered a wash sale.

This creates a 61-day period (30 days before, the day of the sale, and 30 days after).

Example: If you sell shares of TSLA at a $1,000 loss on November 21st, any purchase of TSLA shares between October 22nd (30 days before) and December 21st (30 days after) could be considered a replacement, thus triggering the IRS Wash Sale Rule.

2. Stocks, Options, and Replacement: What the Rule Covers

The IRS Wash Sale Rule covers more than just common stock. It applies to stock or securities, which explicitly includes options.

Furthermore, “replacement” isn’t limited to simply buying the same shares. Replacement includes acquiring the substantially identical securities in a fully taxable trade. Therefore, acquiring an option contract—like opening a TSLA call option—on the same underlying stock within the 61-day loss window can also trigger a wash sale.

Note: The definition of substantially identical securities is often debated, but generally covers the same stock and can include options on the same underlying security.

Short Sales and the IRS Wash Sale Rule

The regulations specifically address short sales: Closing a short sale at a loss and then opening a new short sale on the same security within the 61-day window triggers an IRS wash sale. Experts also interpret the rules to imply that buying the same security–or opening a long positions–could also trigger a wash sale following the close of a loss-generating short position.

3. The Multi-Account Extent

The IRS Wash Sale Rule applies across all accounts you control, regardless of the brokerage firm you use. This means selling a security for a loss in one account and replacing it in a different account within the 61-day window results in a wash sale.

Going a step further, the IRS says the rule applies if the replacement is made by your spouse or a corporation you control. Most tax experts agree this means you must adjust wash sales between all accounts that report activity on the same tax return.

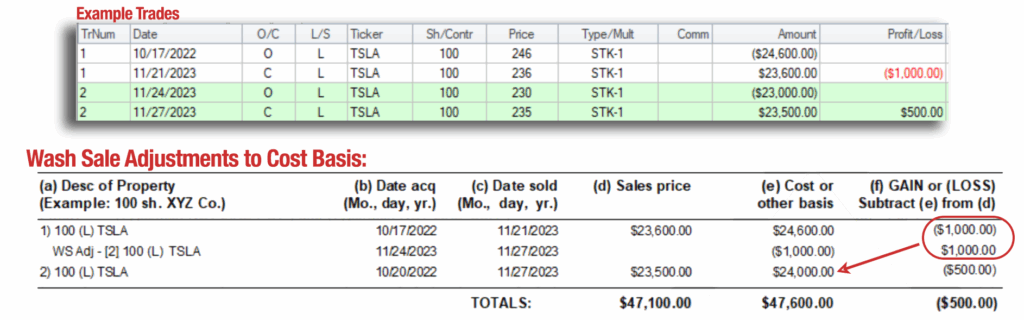

4. Cost Basis Adjustment (Loss Deferral)

When a wash sale occurs, the IRS Wash Sale Rule prevents you from taking the loss immediately. Instead, the loss is disallowed and deferred by adjusting the cost basis of the replacement position.

Continuing the Example:

- You sold 100 shares of TSLA for a $1,000 loss.

- You replaced the 100 shares a few days later, buying them for $23,000 (your actual cost basis).

- The IRS Wash Sale Rule requires you to adjust the cost basis of the replacement position by adding the disallowed loss amount:$23,000 (Actual Basis)+$1,000 (Disallowed Loss)=$24,000 (Adjusted Basis)

The loss is not gone; it is recovered (claimed against future gains or income) only when you finally close out the replacement position (the one with the $24,000 adjusted basis).

Nuances of Cost Basis Adjustment

- Proportionality: If the number of replacement shares is more or less than the shares sold at a loss, the adjustment to the cost basis is proportional.

- Holding Period: The IRS requires the holding period for a replacement position to include the holding period of the security sold at a loss. This prevents you from converting a long-term loss into a short-term loss.

🚨 The IRA Trap: Permanently Disallowed Losses

One of the most financially damaging aspects of the IRS Wash Sale Rule is its application to non-taxable accounts, such as a Traditional or Roth IRA.

If you sell a security at a loss in a taxable account and replace the position in your non-taxable IRA within the 61-day window, it is a wash sale.

The disaster is this: the loss is disallowed, but because the IRA is a non-taxable account, you do not get to adjust the cost basis of the replacement position. The loss is therefore permanently disallowed, which severely impacts your bottom line.

Key Takeaways: Understanding the IRS Wash Sale Rule

To summarize the essentials of the IRS Wash Sale Rule:

- The wash sale window is 61 days: starting 30 days before the sale, and extending to 30 days after.

- The rule applies across stocks and options, and all accounts you control.

- When a wash sale occurs, the loss is deferred (disallowed) and added to the cost basis adjustment of the replacement position.

- Replacing a loss position in a non-taxable IRA results in a permanently disallowed loss.

What’s Next?

While the consequences of wash sales can be disastrous, you don’t need to become obsessed with avoiding every single one. Continue leaning how IRS Wash Sales affect the bottom line for active traders–why you don’t need to panic, and when you do need to be concerned.

Learn More

Go to our WASH SALES Comprehensive Guide

Visit our TRADER TAXES Education Center

Learn how TradeLog helps traders and active investors take control of wash sales.

Please note: This information is provided only as a general guide and is not to be taken as official IRS instructions. Cogenta Computing, Inc. does not make investment recommendations nor provide financial, tax or legal advice. You are solely responsible for your investment and tax reporting decisions. Please consult your tax advisor or accountant to discuss your specific situation.